Hello Meterians,

The Second Incentive cycle on Meter Mainnet started on December 8, 2021. It will end on January 6, 2022.

As the Second cycle comes to an end, we will review the performance of the incentivized pairs and determine the reallocation of volt for the third cycle from January 7, 2022 to February 6, 2022.

This review will also take inputs from the earlier analysis conducted mid-way. The earlier analysis can be found here:

Evaluation of Incentivized Liquidity Pairs:

We could define a few of the critical parameters that will help us evaluate the performance of the liquidity pairs on Voltswap;

- Transaction Volume

- This is by far the most important parameter for evaluation since the goal of the product is to generate free cash flows from the operations and be self-sustainable

- Total Value Locked (TVL)

- This is a critical parameter to gauge the adoption of the DEX. Higher TVL is typically correlated with higher adoption and enables bigger buys on the DEX without too high a price impact

- Turnover of the pair

- It can be defined as the ratio of Volume by TVL

- Higher volume for a specific TVL means that the pair has a higher utilization of assets and the LPs are generating higher revenues due to the turnover.

- Number of Txs and average transaction value

- The average transaction value helps us estimate whether the liquidity available in the pool is enough to ensure the users have lower slippages

- This information is currently now available on Theta Mainnet deployment

Evaluation Parameters;

- The overall role of a pair is a factor of both the TVL it adds to the Voltswap as well as the transaction volume of the pair.

- However, the intent of TVL is to primarily aid transactions and lower slippages, we will try to weigh transaction volume at 65% and TVL at 35% to gauge an overall role of a pair in the growth of the ecosystem

- We will also try to look at the turnover (average 1-day Median Volume by TVL) to determine the capital efficiency of the pairs

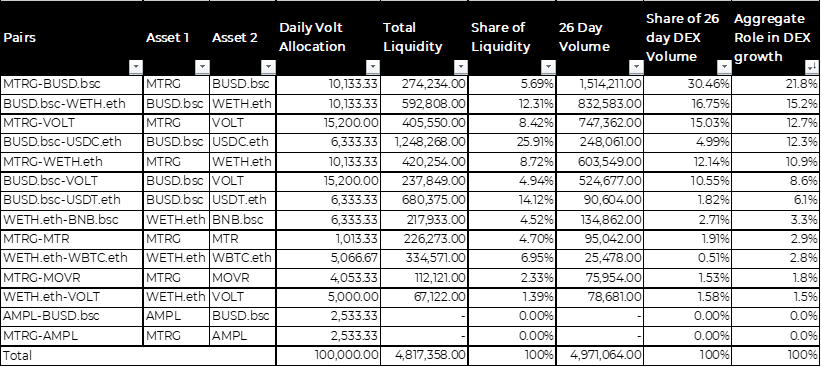

Based on the above parameter, lets us look at the statistics on Theta Mainnet

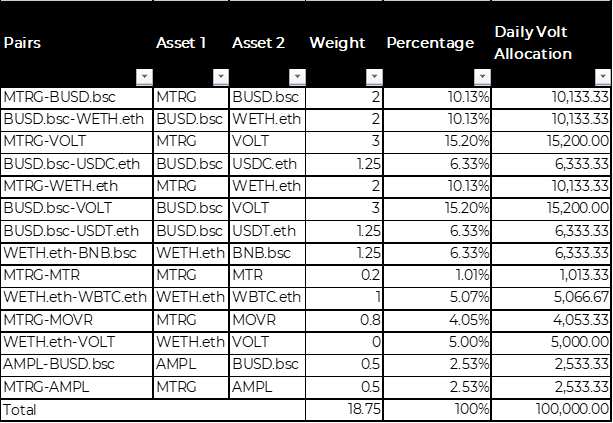

- Current Volt allocation to the Incentivized Pairs

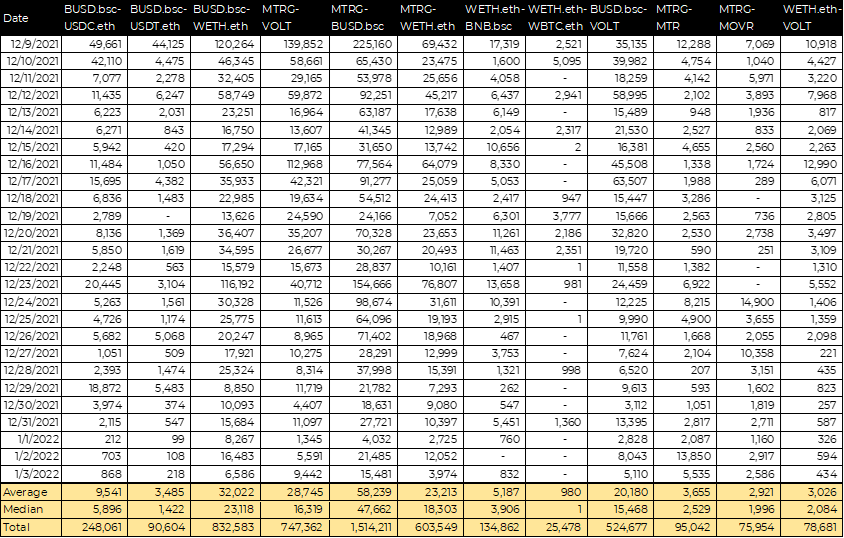

- Daily transaction volume of Incentivized Pairs

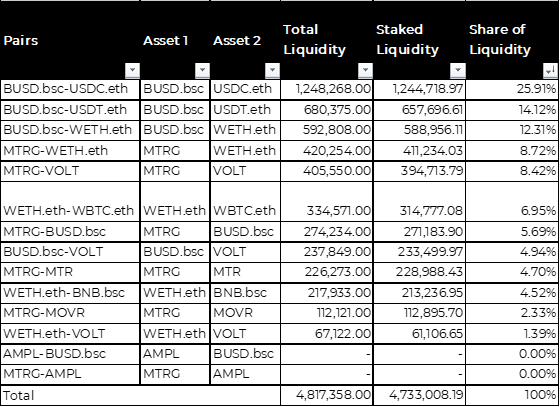

- Liquidity for Incentivized Pairs

- Transaction Volumes for Incentivized Pairs

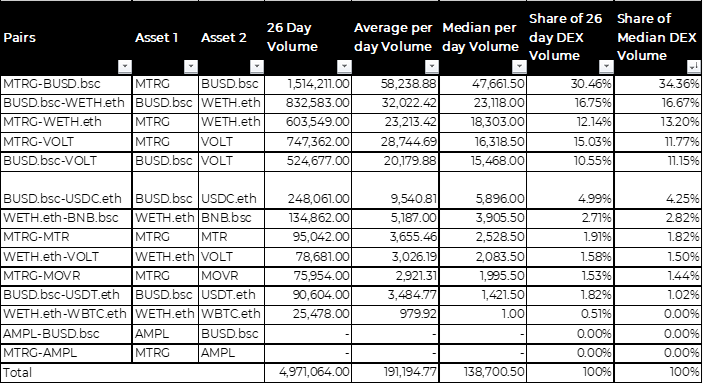

- Evaluation of Pairs based on overall role in DEX Growth (65% weight to transaction volume and 35% weight to TVL)

Insights

- MTRG-BUSD has the most volume per TVL of all the pairs. We can target to improve more liquidity on the pair to enable lower slippage.

- BUSD.bsc-USDC.eth and BUSD.bsc-USDT.eth have both high liquidity but very low transaction volumes.

- Top 5 incentivized pairs have 85% of transaction volume while holding 40% liquidity

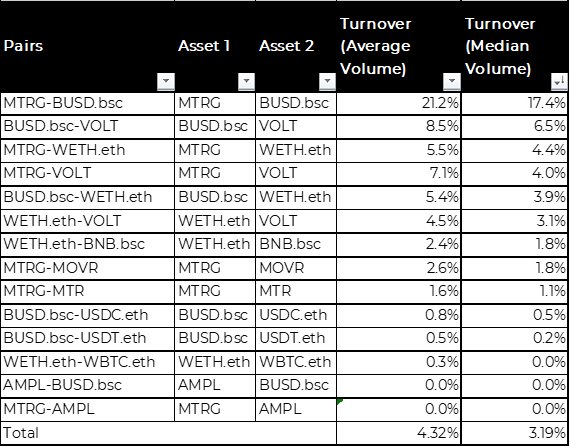

- Turnover (Volume by TVL) for Incentivized Pairs

The turnover data presents another perspective on the insights presented earlier. Stable coin pairs and WBTC.eth-WETH.eth have very low turnovers.

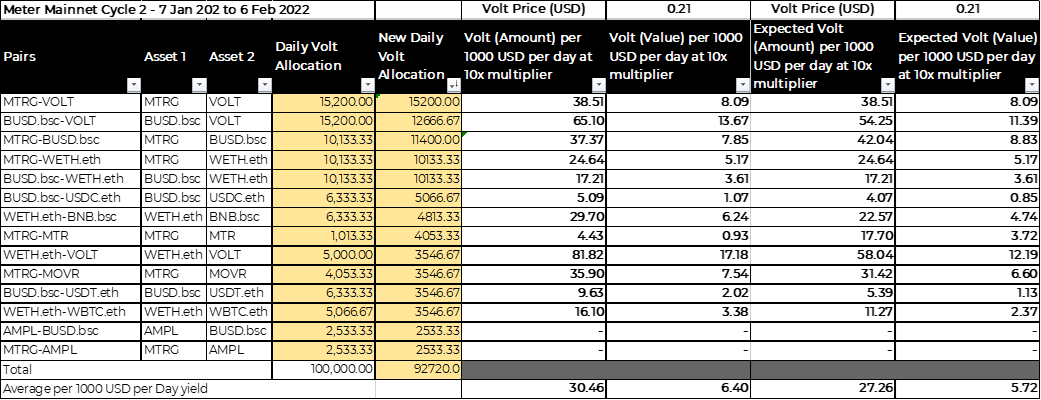

- Volt Earnings per 1000 USD of Liquidity provided

Insights

- BUSD.bsc-VOLT, WETH.eth-VOLT had the most earning potential per $1000 USD of liquidity

- The lowest return is on BUSD.bsc-USDC.eth at around 40% annually.

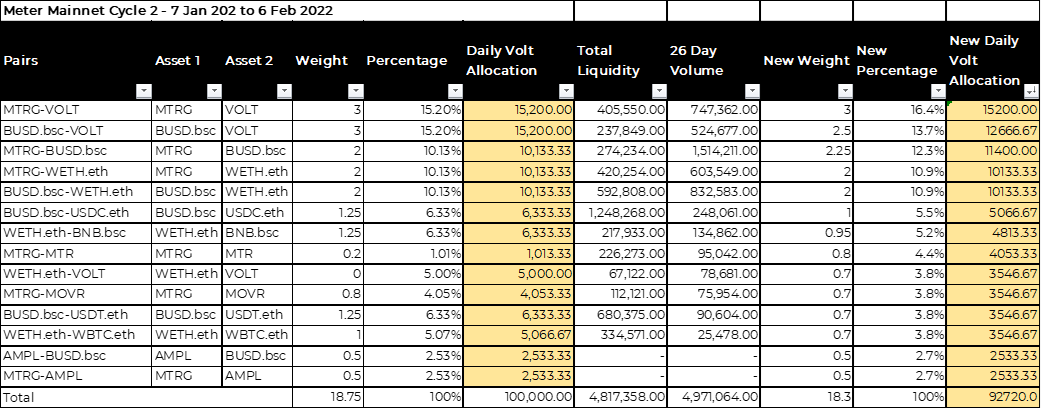

Based on the above insights, the volt allocation proposed for the 3rd cycle on Meter Mainnet are as below;

The Volt Earnings per 1000 USD of Liquidity provided based on new Volt allocation is as below;

Insights:

- Assessing that BUSD.bsc-VOLT has not received traction in the first cycle, the volt emission is reduced. Even so, the pair still remains the highest Volt earnings per 1000 USD of liquidity provided. We expected users to provide more liquidity and deepen the pool further

- BUSD.bsc-USDC.eth has the lowest volt earnings. This is due to 2 reasons – Lower transaction volumes and no impermanent loss

- WETH.eth-VOLT, BUSD.bsc-USDC.eth, and BUSD.bsc-USDT.eth allocations are reduced due to much lower transaction volumes. The volt earnings are still equivalent to average earnings.

- Allocation has been significantly increased for the MTRG-MTR pair from 1013 Volt/day to 4053 Volt/day as we look to deepen the MTR liquidity on Voltswap.

- The estimated earnings are at Volt price of $0.21 USD and Voltswap valuation of $1.9 million USD. The earning potential significantly increases with increased Volt price.

Higher liquidity provision for Volt pools is the key reinforcement driver that will enable increased volt price as well as lower price impacts for users.